Two books that I have recently finished, Mark's The Most Important Thing Illuminated and Neill's The Art of Contrary Thinking highlighted that market sentiment often swings in a pendulum like motion between extreme fear and extreme greed. One way for an investor to make significant gains is to recognise where we are in the market thereby exploiting opportunities as they arise. By and large the most gains can be made when you can keep a cool head and calmly make purchases when the majority of the population are panic selling and selling (or at least reducing purchases) when prices start to overheat. As such, I have spent a considerable amount of time pondering sentiment and relevant indicators and have made the following observations of different gauges.

Quantitative Indicators

Stock Market Price

It would be hard to argue that there is a stronger indicator of market sentiment than the market pricing itself. In stating the obvious, the current price of a stock clearly represents what the market considers to be fair value as at that one point in time. The PE ratio gives a ratio of earnings per share to each share price which in turn provides rough guidance on whether a share is over or under valued. A further step would be to consider the Forward PE ratio to gauge the expected growth and earnings. The higher the Forward PE ratio the higher the predicted growth of the stock which gives a crude starting point for the market's disposition.Relative Strength Index

The RSI is a momentum indicator that provides a measurement on whether stocks are currently overbought or oversold. The calculation for RSI is fairly complex:

N is often taken to be 14.

The result is a number between 0 and 100 whereby 50 indicates that stocks are neither oversold or overbought, a number closer to 100 indicates it is overbought and a number closer to 0 signals under bought. A range between 30 and 70 is considered fairly normal.

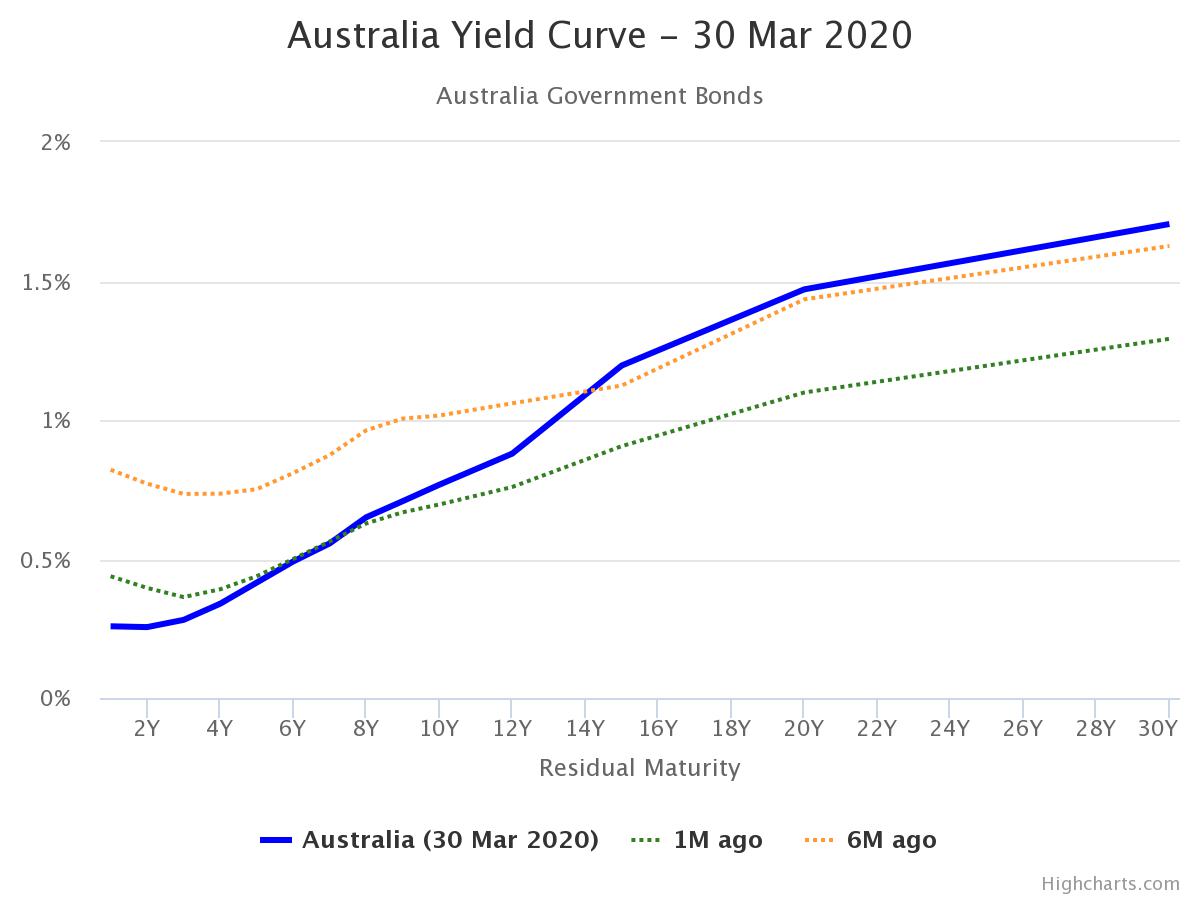

Bond Yield Curve

The Bond Yield Curve has recently been cited often as an indicator of impending recession, however there is far more information to be gleaned from it than just the one omen of impending doom. Going back to basics, a bond's yield tells you what the annualised return is from purchase to maturity. As is with the laws of uncertainty, it is riskier to purchase a bond for a longer duration than a shorter one (because you can never really know for certain what will happen in the longer term future) and accordingly in normal situations long term bonds will tend to attract a higher yield than short term.For reference, our current bond yields in Australia are as follows:

Our current yield curve looks like this:

Different orientations of the curve give different hints to what can be expected in the future.

Normal Curve - has a lower short term yield with a mild increase to mid term and long term. This indicates a normal level of confidence about the future.

Steep Curve - has a lower short term yield with a much greater mid and again much greater long term yield. It is a very bullish signal and has historically correlated with rallies in the stockmarket.

Flat Curve - indicates a lack of investor confidence in the future and is a moderately bearish indicator, although not as bearish as the inverted curve.

Inverted Curve - occurs when short term bonds produce a higher yield than long term bonds. This demonstrates that investors are expecting a drop in yields over the long term as well as a high risk in the short term. This is a very bearish indicator and is often portrayed by the media as a sign that a recession is imminent, whether or not that is true is another matter for a separate debate.

Qualitative Indicators

Pendulum of Hysteria and Euphoria - Changing times?

Moving away from the highly technical quantitative indicators, I find that having an understanding of investor mood through qualitative signs is also important in pinpointing where we currently are on the pendulum swinging between hysteria and euphoria.

There are a number of sources that I have referred to, each with their own limitations. The news is an obvious starting point but the media always sells more by playing up the fear factor, so this often ought to be taken with (at least) a grain of salt. Friendly conversation with friends and coworkers can also provide insight into what your peers are thinking, but of course you are narrowing down your sources to your acquaintances which may only represent a small segment of broader society.

A resource that I have found somewhat insightful over the years is Reddit, specifically the subs investing, fiaustralia, ausfinance and wallstreetbets. Although you are also limited to a demographic of people who are clearly computer savvy enough to post and engage with the online community, it provides a less biased account of reality.

A snapshot of some posts on Ausfinance today results in the following:

As mentioned above, we have since experienced a considerable uptick in the last week and the posts in the screenshot provide a good indicator of how the typical retail investor is reacting to this market movement. From hope of a bearish future with the prospect of incoming defaults and further falls anticipated in equities to the user who invested his whole life savings into BBUS and BBOZ it is clear that they are all anticipating further falls in the market. Whether or not we have reached the extreme end of the pendulum is anyone's guess but these posts seem to indicate that even if we haven't, we ought to be fairly close.

Another interesting note on the matter though, traditionally retail investors were not sophisticated enough to buy inverse indices or puts as these products have only been made available to the masses relatively recently. I would suggest that with these products being made available, an adjustment to our pendulum ought to be made to reflect this, since once the market has clearly taken on a downward trend, euphoria can be found in retail investors who have bought inverse indices or puts where traditionally there would only be hysteria. It would seem that now hysteria only really arises when the market turns and those who missed the signals are caught like a deer in the headlights.

Keynesian Beauty Contest

One final qualitative measure that I will touch upon today is the Keynesian Beauty Contest. For those who are unaware, rather than the traditional beauty contest where participants are asked to choose who they consider to be the most beautiful, they are asked to choose who they think will be voted most beautiful, i.e. crowd consensus. In other words, it constitutes a game of sentiment whereby the winner is the person who can guess better than the crowd as to how the crowd will behave.In applying this back to our current situation with Covid and the lockdown that I find myself in, we have seen not infrequent headlines whereby the crowd has bought into the hype that the shutdown that we face will be ongoing for months on end, tens of millions of people around the world will die from this virus and the markets will never recover ever again. The most important question though is that although this is what the crowd believes will happen, is this likely to be a realistic outcome given our fundamental understanding of human nature? I would argue that it is not.

In closing, I would like to round off this post with some words from, Warren Buffett, “Be Fearful When Others Are Greedy and Greedy When Others Are Fearful”.

by 小福

No comments:

Post a Comment